|

Who or What are you supposed to be leading? Not all levels of leadership's focus should be directed at leading the people, it sounds crazy, but it is true. Depending on your role in the company or where you are positioned, your leadership may need to focus on a different subject area that does not directly involve people; but instead involves processes, thoughts, analytics, and strategies. What we are talking about is the leadership of the company itself. Why would you want to direct your focus on leading the company, and how would you do this? The company's leadership focuses on different aspects of the company, for example, where the company is now, where it wants to be, and how it will get there. You will want to look at where the company is now and analyze what is going on both internally and externally. You will need to ensure that you can define the company and make sure you have built the foundation of how you will get the company to where it needs to be. If this is done right, the results of leading the company will set the standards for management teams so that they can lead their teams effectively, efficiently, and, more importantly, within the parameters of the company to reach the goals set forth. Leadership is about inspiring, encouraging, and ultimately goal achievement. We have to remember that a company is an entity, and without actions taken, molding, or inputs, it will not grow, change, make movements forward, have a set standards, or defined goals. Just like a team or people, it has to be treated like a living, breathing thing, just as you would your employees and teams. When leading the company, the focus changes; one is no longer directly motivating people to achieve a common goal, but instead, we are defining the goals, identifying what is important to the company, and setting the standards so that down the line, leaders can be motivating and inspiring to achieve the common goals. This is accomplished in various ways; the starting point to this leadership attacks the tasks given to the company by analyzing the company's strengths and using them to identify opportunities and then capitalize on them. It is about acknowledging the company's weaknesses and improving them. We can not forget about combating both internal and external threats. Additionally, you will need to ensure that your mission, vision, and values are true and accurate to the company. These are reference points and foundations for how and why the company does what it does. They are also guiding points for strategies, cultures, and the future. There are many leadership styles; each type has a purpose, a time to be used, and individuals with particular skills and traits that can execute. When discussing leading the company and specifically the points listed above, a strategic leadership style will help to accomplish this. Because leading at this level is about being strategic. Additionally, strategic leadership has a focus at the executive level and a pass-through to the line level. Strategic leadership of a company is designed to produce multi-fold results at the business level. It will increase productivity, optimize processes, create a clear understanding of company goals, how to get there, define the company, and identify what is good, where opportunities are, and how to execute. By doing this at the company level, the effects will trickle down and set the standards that will allow others to lead the people, encourage them to meet the goals, define the culture, and enable employees to be independent within the company parameters to use their thoughts and ideas to accomplish goals allowing them to execute their roles to get the company where it wants to be. You see, the company is the foundation for everything. It is the leader of everything that it encompasses. The leaders in the company cannot lead to the common goal if the company is not defining, analyzing, finding, and executing opportunities so that others have a direction. AGDA Consulting

0 Comments

Inflation is at an all-time high, gas prices are skyrocketing, stocks are dropping, interest rates are up, and my dollar is not going as far as it used to. So what happened, and how am I going to get through this? These are all questions that many businesses and families are asking themselves right now. Despite just going through a multi-year pandemic, the economy was doing pretty well. Some particulars can be argued, but in a general sense, things were good, and then this, today we are seeing a different economy leaving many wondering what to do. An appropriate initial response is to control spending and budget to ensure that you do not let yourself create debt that could have been avoided. Then is the big one, the step that will help ensure you remain sustainable and come out of this economic slump in good standing. That is to make a strategic plan for the next few years. If you own, manage or direct a business, this is a must and something you can also do for your personal life. This will be a very tough future for some companies; some will prosper, and others will remain constant through these times. Each business has its own external factors that affect its internal operations, which will determine your industry’s future outlook. It is important to remember that the external factors will ever be evolving, creating new causes and effects on your business, so you have to keep up with what is happening that relates to your business. For some companies, this might be the first time you start to examine all the pieces that go into what it is you do and how they affect your outcomes. By reviewing them, you will not only be able to adapt to the now but will be an even better businessman in the future. What is a strategic plan? In the simplest terms, it is identifying where you are now and where you want to be in the future, then creating goals, action steps, checks and balances, and a thought-out plan for getting there. Everyone’s current position and goals will be different. More importantly, everyone will have a different vision of where they want to be in the future. Examining and analyzing external factors or possible threats, like, the stock market, supply chains, local economies, and cost of goods, just to list a few, will help to identify factors that will influence the steps you will take to meet your goals along the way to where it is you want to be in the future. You will also want to identify your strengths and weaknesses to maximize your efforts when taking steps to reach your goals. We must remember that there are opportunities that can be found in bad situations, which can help guide your company on where it may want to be in the future. Most importantly, you must be able to identify where you want to be in the future and how you want to take your company. Without this, you will not have a target to aim for, and something to be accountable for, that will help keep you on track. In addition, you will want your thoughts and actions working with a purpose so that you are not making spontaneous moves that lack reason or a defined purpose that will not create value. These will help give a foundation for you to ensure you get to where you want to be in the next few years and a proactive move to what is happening now.  Knowing the standards in your industry is one of the fundamentals that will keep you competitive. It will help you identify areas of weaknesses, see your strengths and notice any opportunities the company may have. So what are some of the standards you need to keep up with regarding your industry, and where do you need to focus your energy to remain competitive is a good question. There are many places to focus on, and each one will provide you with some insight and give you something to measure against. Having something to measure against gives you a standard to compare your company to, and two great ones are gross and net profits. These industry standards tell you if you are doing ok and meeting the norm for that industry. This is important for small businesses because they need to know that they are making the money they are supposed to make and are competitive within their industry.

The gross profits or gross margin is the remaining money from the total sales revenue after subtracting the costs of goods sold (COGS). The COGS are just that, the cost of what it takes to make your products or provide your service. The COGS typically includes the materials and labor it takes to make the final product. The word gross tells us that no other expenses have been taken from the total revenue at this time and lets you know what is left over to pay additional costs. The gross profit does not directly tell you your overall profit, but is a significant number to examine and compare to industry standards. We suggest that you segment out your COGS to get a better set of numbers to analyze and look at it as percentages of total revenue. Comparing this to industry standards is very important. It can tell you if you are competitively priced, paying too much for the raw material, your levels of waste from the raw material and labor, and how efficient you are in making your product. When looking at a profit and loss statement, it can tell you if you are sitting on too much inventory and have a poor turnover or bad purchasing patterns. This is because a P&L does not account for inventory on hand. Having high inventory means having money on the shelf, lowering your cash flow, and limiting other opportunities where that money can be doing something else or making you more money. The gross margin's nature allows an owner to see how well they are doing operationally compared to an industry standard and where they need to focus efforts in the operations to be better and more profitable. The net profits are the bottom line or the company's money when all expenses have subtracted from the total revenue. This needs to include the owner's pay if you are a sole proprietor. When it comes to industry standards, the problem is that not all data takes the owner's salary into account and gives some skewed results, but it still provides us with a percentage to compare to and make decisions. Here at AGDA, we typically advise that net profits be as low as possible after knowing a company is meeting the industry standards, because that means that the company is spending money on itself to better the company. That is why it is key to be competitive with industry standards. It tells you that the company is making the correct money and can do other things. Your net profits are what is leftover. That money is what can be used to expand your company or reinvested back into the company to make the company, product, experience, or presence better. It can also be used to beef up cash on hand for additional opportunities. If this number is below the industry standards and all other areas are in line, it tells us that sales levels are typically not sufficient, and focus needs to be on increasing sales or why the sales are not enough. It can also tell us that costs between gross and net profits are too high or not in line with current norms. Every situation is different, but you want to be able to compare to the industry standard to see if you have a sustainable business and if line items are appropriate. We have to remember that meeting industry standards are measurables that let you know where you stand compared to others in your industry. Operating within the industry norm tells you your performance against the norm, but these numbers can change with innovation and markets. If you can find innovation, you can increase your gross profits. For example, when Ford introduced the assembly line, an innovation was found and increased production time and lowered labor costs, giving a better gross profit, allowing the company to have more opportunities with the remaining cash. On the other hand, when the cost of a product goes up but a market does not allow for the sale price to match or revenue decrease due to an economic situation, and a business does not adapt to meet the industry standard, both the gross profits and net profits decrease. Overall if you know your industry standards and can meet them, you can then make decisions faster to stay ahead of what may happen. You can also find ways to make your company more profitable, whether through reinvestment or increased cash on hand to be used and distributed as the company deems appropriate. Most importantly, you know that you are making the money you are supposed to be making.  Leadership has become a hot topic amongst younger generations in the workforce. As the need for effective leadership continues to trend upwards in the workplace, so has the rise in social media posts that focus on leadership as the main driving force of an organization's success.

While leadership is essential in all aspects of life, from recreation to business, and is crucial for any team's success, other factors contribute to a company's success that should not be overlooked. The simple definition of leadership is guiding or influencing others to reach a common goal. One could also view it as a manipulation of group members who lack the strength to achieve a common goal independently. Either way, the goal of leadership is to get a group of people to work together to complete a task that benefits the desired need. Partnering people who lack certain skills with people who have those specific skills can help the skilled persons master styles of leadership that the others will buy into. On the business level, this is the simplest act of leading people for the company’s best interests. The other side of business success is management. Yes, I said management. "Management" has almost become a bad word in the minds of many because of its negative connotations. Because of this, the term management is often pushed aside and replaced with "leadership," which provides a different connotation. If people think they are being "led," it makes them feel good. However, if they feel they are being "managed," it feels demoralizing, and this is where the problem starts. Being managed still means being led. Someone has to take charge. A manager or boss, has an essential job. When a manager does not do their job correctly, there is nothing left to lead. Management is the controlling of assets and resources by planning, organizing, examining, thinking, directing, and leading to create success for a business and its shareholders. We have to recognize that without management, there is no leadership. Without a boss overlooking the entire situation, using multiple sources of data, knowledge, and experiences, the leadership has no direction. The role of management is much more than the leadership of the people. Management is the leadership of the company. People in management are required to examine many different influences beyond simple directional leadership. Managers must see all sides of the process and make decisions that will set the foundation, so that those who lead and follow can be successful. If management is such an important part of a company's successful operations, and is a foundation for leaders, why is it such an undesirable term? We can dissect generational traits, or blame the organizations for not putting better managers into their roles. We can try to prove that pop culture has helped contribute to some of management's negative connotations. We can also say that the use of social media and freedom of choice has closed our minds and limited our thoughts to expose ourselves only to the media that conforms to our personal views. We can even blame the people who saw the need to make a good business move while exploiting a specific style of leadership or management that appealed to their followers. Any of these could be contributing factors. In the end, everyone in the business world could benefit from being educated on the basic principles of leadership and management to see how everything ties together, and identify key components to overall business success, rather than just their own personal wants, or goals.  The term "Think Outside the Box" has become a normative phrase that is typically used to initiate creative thinking amongst a team when addressing a problem, finding innovations, or motivating thought. It is also sometimes a crisis response method in hopes of a quick fix. There is nothing wrong with this practice, and it can, at times, lead to innovations or solutions when used correctly.

However, this approach may be preemptive or a desperate reach for a solution that requires a different approach and does not produce the desired result. It can sometimes be misinterpreted as a solution, but in reality, it was not at all the action that should have been placed into the team's minds. There is another fundamental thought that can be used and should be considered before letting the preceding statement be said. It does not sound as fun, but it is much more practical and probably needs to be what is addressed. That phrase is "Get Back in Your Box." Every company has its own box. That box is composed of things you hold of value and how you want the company to be operated. It is what guides, motivates, and gives you pillars to stand. A strongbox should consist of mission, vision, values, culture, goal, and policies. These six sides of your box are what frames your company. They should guide all your decisions, influence how you think, and conduct your business. Sounds simple enough, and one may say that sometimes you need to leave that box to find innovation, and we would never argue that thought had the situation allowed for that. The problem is that even though you have this box, you are not fully utilizing it and harnessing all of its potentials. You are not maximizing its values, which were at one time used to get you to where you are now. You have probably moved away from some of these guiding factors or have not adapted them over time. Your core strategy has just become something of the past and is no longer a strategy. Let's look at a well-known company and, more particularly, at the point when the leader was forced out of the company. For years this man did an outstanding job at building his box and sticking to it. He made a company that thrived in market share, innovation, culture, and profits. When the board removed him from the operations, they took the "let's think outside the box" approach. They wanted to change the box instead of using and refining it. They kept trying the think outside the box, over and over, and because of this mindset and direction, they destroyed the company to the point that the former leader, the one that built the box, was brought back, and he immediately reimplemented his box. Why did he do this? Not out of arrogance, but because he knew the value of the box. He knew that the fundamentals of the box had gotten them through tough times. It had led them through times of need and product development. It was a solid and sturdy box, and he stuck to it, knowing that it would always support the company. Now, this example only outlines one scenario, a scenario built around a person who knew the value of his box and how to use it. Someone that never abandoned the box and did not need to be reminded to get back in it. But we need to realize in this example that the box was always the answer, and when the company started to try and think outside of it and change it, they started to encounter failure. They did not have guidance or anything to influence thought and decisions. Their pillars had crumbled because they were being re-engineered with poor choices. As a leader, before you speak the phrase "think outside the box," take a step back and analyze your current task using your box, especially if you have already had success with your box and see what has happened to your box or how it is being utilized. Is there a weakness in the box? Have you moved away from your box? Are you utilizing all the tools in your box and utilizing them in the way they were intended to be used? There is a good chance is that you are not. If that is the case, then it is time to get back in the box and start to remaster and strengthen who you are, what you do, and why you do it. Now, to get back in your box, if you have moved away from it and are thinking about saying the phrase, "let's think outside the box, " you need to make sure that you keep your box fresh. Repaint it, touch up the corners, and fix the dents, but do not leave the old box for a new one. If you take care of it, you will never have to leave it, and if you use it, the box will always support you and give the boost you need to see over everything else. Thinking outside the box is a way to approach a situation, but it should not be the 1st thought that comes to your mind and the direction given to your staff. It is needed at times, but if it is a desperate lunge for a quick fix or a shortcut, you will not get where you need to be or want to be. Take time to reevaluate your current situation based on your box and how that box has supported you all along. Determine how it can provide the answers you need. Then use it to stand on, be your support and foundation to the situation you are addressing.  Never before has the workforce been made up of five different generations. That is right, five different ways of thinking, five different groups of people that have been exposed to different life-defining events, and five different ways of seeing a solution to an issue. This presents many differences for a manager, leader, or business to be aware of, manage, and lead.

We can all admit that we have heard or said that certain generations just "do not get it." There is some truth to that statement, but only to the person who thinks that and the person who does not understand other generations. A generation comprises a group of people who share a certain time frame and specific traits attributed to that group. That is typically where most people stop. They see the age and the traits of that group and leave it there. As a leader, manager or business owner, one has to go further into what a generation is. Managers and leaders have the responsibility to understand each generation, see their value, weaknesses, what traits are shared across other generations, and most importantly, what caused them to have that trait. A more detailed definition of a generation is a group of people who share specific traits that were developed during their formative years, caused by specific life events which were unique to their time. As a leader, you can find the value brought to the table by your team members if you can understand that. Leading different generations is not an easy task to do. There are many different personalities and viewpoints that have to be managed. It can be frustrating at times, and specific team members may appear to be more of an anchor. It does not have to be this way though. You can have teams of different generations and have great success. Successful leadership is accomplished by being able to lead a team to the desired outcome. That means you have to be able to adapt. You have to have a more extensive skill set than your followers, and you have to be able to identify, pull and mold it all together. Do not take this as you have to accommodate for individuals because as a leader, you challenge and guide them, you do not accommodate. In today's world, having a more generational diverse team is an asset. Each generation has specific skills and valuable viewpoints. Technology moves parts of your business faster than others, and the younger generations are entuned with the technology. However, the older generations hold knowledge and values that can only come with experience. How do you make a team that is generationally diverse and will be productive? Before you try to put the team together, make sure that you have your cards in order first. Know your mission, vision, and values. Aligning the team with the company's mission, vision, and values has nothing to do with age or generation. It has to do with the individual. When you build your team, you must build it with members who believe in, buy into, and demonstrate the company's mission, vision, and values. By building a team that shares these common core business practices, you already have pillars for a great team. Be able to communicate your strategy, know where you are, what you want, and how you plan on getting there. Like the mission, vision, and values, this is a belief that if you can clearly communicate to your potential team members and find the ones that can get behind your strategy, it again will not matter what generation they come from. Now that you have narrowed down the potential candidates, you have to acknowledge that each generation has something to offer and that you as the leader will need to harness that. You also have to create a culture of mentorship and reverse mentorship. One thing that all generations share is they want to be valued, and they want to learn. The use of mentorship and reverse mentorship opportunities can create an environment that will allow for these valuable tools to be used. It will also give excellent groundwork for developing respect and acknowledgment of other generations and their value. This will allow one generation to see that other generations' ways and skills also have value and are crucial to success. Traditionalists, the oldest of the workforce, are loyal, grateful to have a job, and believe in top-down decision-making. They believe in the organization, have strong work ethics, and exhibit accountability. They strive for clear communication and collaborative work environments. Baby Boomers live to work, are loyal, have an attachment to authority, traditions, and culture. They are self-motivated and resilient to change. Success is vital as they are motivated by position, income, and reputation and are willing to sacrifice. Additionally, they have respect for other's autonomy and communication. Generation X was the first introduced to technology. They are more diverse, self-defined but have a lack of loyalty to employers. They are very willing to conform to social norms and traditional values but are less competitive and more collaborative than other generations. Generation X prefers relationships over authority, and they thrive on challenges and change. Millennials prefer being pulled together by a leader and have a desire for change. They exhibit more assertiveness, narcissism, and self-esteem. They are very team-oriented, multitaskers, and strong with technology. This generation has a want for learning new skills and thrives on recognition. Generation Z is the most useful in the technology world than any other generation. They prefer freedom and individualism for their projects and, in turn, are not key on teams. They are very achievement-oriented, highly educated, inexperienced, but very diverse. As we can see, each generation has its traits, and in general, not all, but many people from these groups have predominant behaviors from the list. Leaders and managers have to see this as what it is, a diverse group of different skills, knowledge, and attributes. A large amount of research has been conducted on this subject. They all agree on one thing. Different generations can disrupt the workplace, but different generations can also be harnessed for the company's good. How we harness it and how it can make your teams and company better are for a different conversation.  Being on the top of a company is not just a power spot or a spot you hold on an organizational chart. It is, more importantly, a strategic spot, an actual place that you position yourself. You are on the top for a reason. Yes, it is because of your title, your accomplishments, and what you contribute. However, it is also a very forgotten mindset of where you need to be when looking at the company, the operations, disruptions, and opportunities. You are on the top because you need to be looking down on the company. As the leader of a company, you need to position yourself so that you are not stuck in the mix of everyday operations. This is a common practice of small and mid-sized operations. These companies' operators, owners, and managers get a mindset or a routine that they have to be in the mix to accomplish anything. However, the truth is that you can only do very little when in that spot. You will end up developing forward sight, meaning that you only see what is in front of you. Resulting in reacting to just that what you see at that moment, in your vision, and making narrow vision choices. If you are looking forward, you are not able to see the entire picture. You cannot see how all the parts are working together or how the problem you see may be a product of something that is not even related to what is in front of you.

By looking forward, we are referring to a familiar role that many small and midsized company owners fall into. It is when they are stuck in the business doing daily operations, putting out fires, making knee-jerk choices, and being reactive to their surroundings and situations. They end up not seeing the entire picture, but only what is in front of them at the moment. This forward-looking is detrimental to the business, the moral of ownership, and eventually the team. Every bit of growth and momentum the business and the owners started stops; it eventually becomes survival mode, every day for everything. By looking down on the business, you have opened your field of view. You have strategically placed yourself in a decision and problem-solving position and are no longer focused on what is just in front of you. You can see the how's and whys of situations. The opportunities start to present themselves, and solutions for problems begin to be easier to see. Your dream and passion begin to become something that you can now develop into why you are doing what you are doing. This step up and out, is one of the most challenging developments most owners have to learn. Those that do and master it become leaders of their company and move the business and success forward. Those that don't remain to look forward, resulting in slowed or minimal growth and eventually burnout. Here are a few steps that can be done to facilitate how you look at the operations Have and use strong policies and procedures - I am sure that we all have an employee manual, but do you have a managerial manual? Do you have a policy and procedure manual? We get stuck in the daily operations because we hold all the knowledge and have only halfway communicated it to our teams. Empowerment – You have hired people to do jobs, so let them do their job. This is a hard thing for some owners to do especially as they start to grow and have to focus their attention on issues that are more related to their level as an owner. Training- Take the time to create and implement a good training program for all positions. Not knowing your position – As the leader and owner, you were not given or told your position in the company, and it depends on you to find it. Not knowing your costs or having a budget – Take the time and run your numbers so you can make educated decisions. Not having strategic thought and planning – Put plans in place that are centered around strategic thinking. If you do not know or understand strategic thinking and planning, learn it. Use resources- Do not be a know it all, recognize your weaknesses and where you have holes in your abilities, and get help from outside resources. The steps that we mentioned can all be done, and getting you in the position of looking-down is very attainable. Call us, email us, come by the office to have a quick meeting, and help you see where you are what we need to get you there. Our mission is to create partnerships that use strategic thinking to continue our client's success.  As business owners, executives, directors, or managers, time is our limiting factor. Needed time is too often take away by disruptions or distractions. At times it can feel like everything is getting done, except what is required to get done. It can be exhausting, and it can beat you up mentally. If it is too often a situation, it can create a box you get stuck in, and eventually, you are just trying to get through the day.

At a certain level or some point along your journey, this will happen, and it will either make or break you. You will either learn to handle it and control it, resulting in moving forward or getting stuck and eventually regress. That is where Investing time to make time comes into place. Suppose you are already in the thick of not having time. In that case, this approach will seem like something that will only make things harder, but you will start to see progress and start to get ahold of your time in reality.

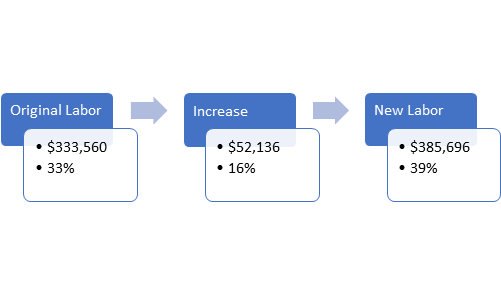

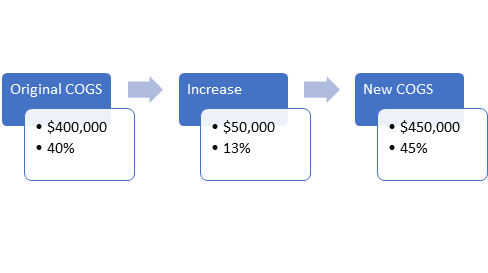

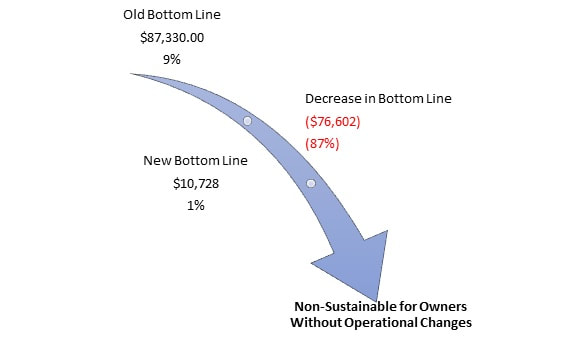

Whether the minimum wage increases or not, you need to have a plan in place. Companies prepared for the changes will see less of an effect on their bottom lines. The companies that will see the most significant impact will be small to mid-size operations on whether they will remain sustainable. Larger companies will be affected by the increase but have more depth to absorb the hit. Every industry is different. Some are more labor-based than others and some are more product-based, but either way, there will be an impact and you must be ready for it. This example is based on a company with an average pay of $10.00 per hour and is now facing an increase of a new $12.00 min wage. This will be a 20% average hourly increase. We have to acknowledge that the 20% average increase would have to be applied to all hourly staff. If someone was making $9.00 then was overnight bumped to $12.00, what do you do to the person making $12.00? You will have to bump their pay as well. That is why we will say that there will be an increase of 20% for all hourly wages. We will also be increasing management salaries, but only by 9% for this example. Before getting too far ahead and thinking that my company already pays everyone at least $12.00 an hour and this will not affect you, you are mistaken it will. For example, if employee A, who does not receive a pay increase due to already making the new minimum wage can get paid the same or close to the same for doing a less skillful, stressful or easier job, how will you retain them? There will be a cost. You will see that there is also an increase in COGS. It would be best if you recognized that there would be an increase in this area. Like you, your suppliers have increased their operating costs. To remain sustainable, they will have to increase their prices and pay the difference. Changes to Labor  As we can see regarding labor, there was an increase of 16% to reach the 20% increase in hourly employees' wages. The 16% is composed of a boost to hourly wages, salaries, and employer-paid benefits. Changes to COGS  Fixed Costs Fixed costs were held constant, like Occupancy Costs and other fixed costs. We should note that it is fair to say there is a strong potential that there would be an increase in these line items. Bottom Line What does this do to the bottom line? The company we are using has a top line of $1 million in revenue. Before the increases that we applied, they showed a roughly 9% return after a 25% tax rate. After the increases, we have associated with the change in minimum wages, their new return is only roughly 1%, an amount that is no longer sustainable. Changes to the Bottom Line  Now What?

That is where we can help you see what you will need to do to remain sustainable. Remember having a plan and looking at hypothetical situations will set you up to be successful for the future. If you wait for the change to come, it is too late.  Increasing top-line sales are a constant goal for every business, as it should be. As sales increase, the potential for other opportunities become a possible reality. Growth on the top line adds value to the company; it will allow the company to grow, create new departments, expand in marketing, do new R&D, and add to the bottom line. One of the issues we run across with top-line growth is that the bottom-line does not always grow appropriately. It is a common oversight and can easily be missed if you are too wrapped up in the daily grind. The business does not have depth in your management team or at director levels or you as an owner have not been taught to recognize this. It can come from a lack of vital budgeting, knowledge of costs, P&L analytical thought, foresight, or acting reactionary. The oversight can all be eliminated with strong operations. Operations are the heart of the company and dictate how everything will happen. If the operations are well put together, you will have known all of what we mentioned above. You will also have already had plans in place and forecasted it out. Let us look at an example of this scenario. This establishment’s fundamental background is that it has successfully operated with profitable growth and a solid business base. The owners are very involved, but involved at the wrong level and are acting more as employees and not as owners. Many critical steps along the way of business development have been missed. However, they have never been a concern because there was always a profitable bottom-line. They made money, so all must be right. Because of their involvement, they never fully completed budgeting, standards, training, or operational manuals. They floated on, “we made money,” so we must be doing great and have everything right. This mindset is common, and if you own a small or mid-sized company, it may be starting to sink in as you are reading that “yep” that is how we do it.” This company’s business starts to grow at a good pace. The top-line is increasing steadily, and so is the bottom-line, and the owners say all must be good with everything. But is it perfect? Is it right? Is the bottom-line reflecting the number that it should be? Are the owners making what they really should be for as hard as they are working? The answer is probably NO. I will get asked, how is this so? Both lines increased, we have more transactions, and we are making more. But the question is, how much more should you be making, and the answer is always “I don’t know.” Another question is, how much money was wasted or opportunities lost in the process of adding to the top line? Lastly, were you as an owner positioned right within the company as this was all happening? Again, usually followed up with another, “I do not know.” The “I do not know” answer is one that can easily be changed to definitive, data-based answers. One that puts you in the position to lead the company and your teams. You have the answers. You can see the problems. You have the solution and measurables. You see opportunities and are making strategic plans to capitalize on those opportunities. Do not be the “I do not know” owner, and do not be the owner that leaves money on the table. That money cannot be picked up, it is lost forever. The missed opportunities cannot be capitalized on, and they too have passed. Position yourself correctly, set yourself up correctly, and maximize everything that you can in your company. By doing so, as the top-line grows, you ensure that your bottom-line will reflect what it is supposed to.  |

AuthorAGDA Staff Archives

March 2023

Categories |

RSS Feed

RSS Feed

Photos from wuestenigel (CC BY 2.0), Ivan Radic (CC BY 2.0), focusonmore.com (CC BY 2.0), wuestenigel, Ivan Radic, kla4067, Carl Graph, nineball2727, Austin Community College, Rawpixel Ltd, gidlark, focusonmore.com, ldifranza